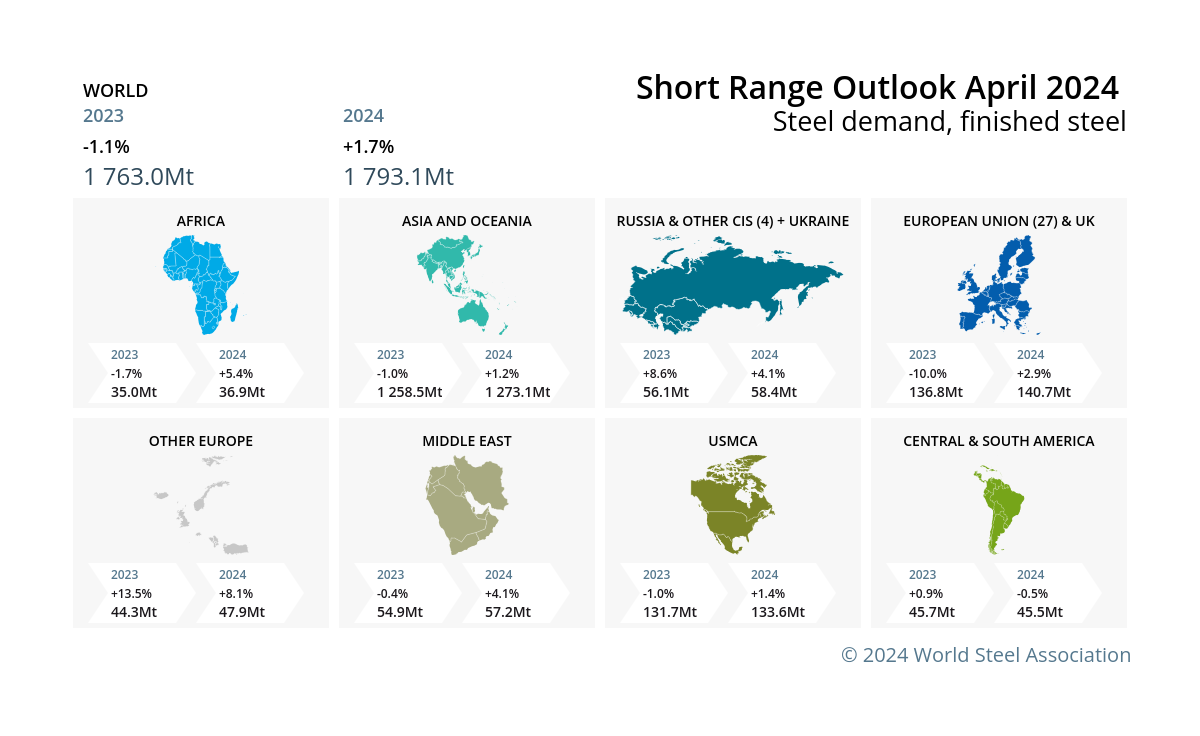

April 2024 | The World Steel Association (worldsteel) has released its Short Range Outlook (SRO) steel demand forecast for 2024 and 2025. worldsteel forecasts that this year demand will see a 1.7% rebound to reach 1,793 Mt. Steel demand is forecast to grow by 1.2% in 2025 to reach 1,815 Mt.

Commenting on the outlook, Dr. Martin Theuringer, Chairman of the worldsteel Economics Committee, sees early signs of global steel demand settling in a growth trajectory in 2024 and 2025.

“The global economy continues to show resilience despite facing several strong headwinds, the lingering impact from the pandemic and Russia’s invasion of Ukraine, high inflation, high costs and falling household purchasing power, rising geopolitical uncertainties, and forceful monetary tightening. As we approach the end of this monetary tightening cycle, we observed that tighter credit conditions and higher costs have led to a sharp slowdown in housing activity in most major markets, and have hampered manufacturing sector globally. While it seems the world economy will experience a soft landing from this monetary tightening cycle, we expect to see global steel demand growth remaining weak and market volatility remaining high on lagged impact of monetary tightening, high costs and high geopolitical uncertainties.”

Short range outlook on steel demand, April 2024 © worldsteel

Steel demand in China likely to decline

Steel demand in China in 2024 is expected to remain around the level of 2023, as real estate investments continue to decline. But the corresponding steel demand loss will be offset by growth in steel demand coming from infrastructure investments and manufacturing sectors. The projection suggests that by 2025 China’s steel demand will be significantly lower than the recent peak demand year, 2020.

According to worldsteel, China might have reached its peak steel demand, and the country’s steel demand is likely to continue to decline in the medium-term, as China gradually moves away from a real estate and infrastructure investment dependent economic development model.

For 2023, the apparent steel use (ASU) estimate for China is based on official statistics and suggests a 3.3% drop.

Other regions expected to grow

Conversely, India is expected to see significant growth in steel demand, projected at 8% annually for 2024 and 2025, driven by robust infrastructure investment. In 2025, steel demand in India is projected to be almost 70 million tonnes higher than in 2020.

Other regions, including MENA and ASEAN, are also expected to experience growth in steel demand after recent slowdowns. But mounting difficulties in the ASEAN region, such as political instability and erosion of competitiveness, might lead to a lower trend steel demand growth going forward.

EU facing challenges, US healthy

According to worldsteel, the EU (and the UK) remains the region currently facing the biggest challenges. The region and in particular its steel using sectors are challenged on a multitude of fronts – geopolitical shifts and uncertainty, high inflation, monetary tightening and partial withdrawal of fiscal support, and still high energy and commodity prices. The persistence of these downside factors resulted in a major drop in the region’s steel demand in 2023 to the lowest level since the year 2000 and to substantial downward revisions of the forecast for this year.

After only a technical rebound in 2024, the region’s steel demand is expected to finally show a meaningful recovery with a 5.3% growth in 2025. The forecasted steel demand for the EU in 2024 is only 1.5 Mt higher than the pandemic trough in 2020.

In stark contrast with the EU, US steel demand continues to show healthy steel demand fundamentals. The country’s steel demand is expected to quickly return to growth path in 2024 after a sharp drop led by housing market slowdown in 2023 thanks to strong investment activity, which received a boost from the Inflation Reduction Act and a gradual recovery in housing activity.

Background

The World Steel Association (worldsteel) is one of the largest and most dynamic industry associations in the world, with members in every major steel-producing country. worldsteel represents steel producers, national and regional steel industry associations, and steel research institutes. Members represent around 85% of global steel production.

More information: worldsteel.org/worldsteel-short-range-outlook-april-2024